Governments in the world's largest economies are facing growing pressure from escalating national debts and rising borrowing expenses. This trend is attributed to increased spending demands related to ageing populations, climate change mitigation, and defence initiatives.

New geopolitical developments, such as conflicts in regions like the Middle East, have heightened inflation concerns. These factors are further straining public finances for nations already contending with multiple economic disruptions experienced this decade.

The substantial debt burdens are beginning to negatively impact economic performance, potentially limiting governmental spending capacity and hindering growth. In severe instances, countries could face difficulties in managing their debt obligations.

Across advanced economies, government bond yields have seen a significant increase since the COVID-19 pandemic and the conflict in Ukraine. This rise is a direct consequence of central banks implementing aggressive interest rate hikes to curb inflation.

Furthermore, investors are seeking higher yields to offset the risks associated with holding long-term debt, thereby driving borrowing costs even higher.

The United Kingdom stands out as one of the most severely affected, with its 10-year bond yields reaching levels not seen since 2008, making it the most expensive borrower among its developed counterparts.

The divergence between short-term and long-term borrowing costs has widened considerably, increasing the overall expense of long-term financing.

Additional pressure stems from central banks reducing their bond purchasing activities, while traditional institutional investors, like insurance companies and pension funds, are decreasing their holdings of long-term government debt.

In response, many governments are shifting towards issuing more short-term bonds. However, this approach carries inherent risks, as these debts require more frequent refinancing, exposing countries to potentially higher interest rates.

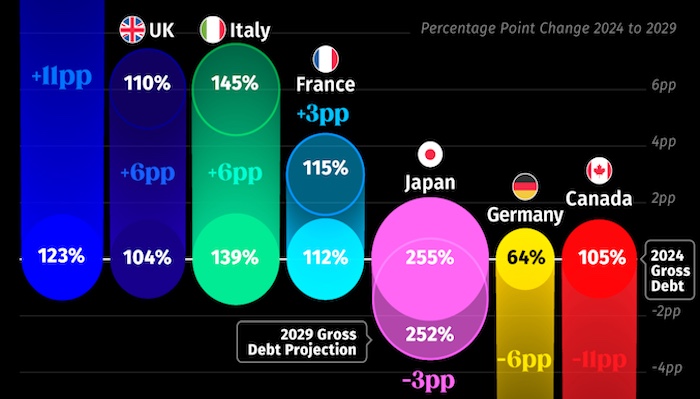

Currently, debt levels in most G7 nations are equivalent to or surpass their gross domestic product (GDP), with Germany being a notable exception among the major economies.

Previous economic crises, including the 2008 financial meltdown, the European sovereign debt crisis, and the recent pandemic, have all contributed to the accumulation of debt and slower economic growth.

Japan continues to hold the highest debt-to-GDP ratio, exceeding twice its economic output. Meanwhile, Germany is increasing its borrowing to finance defence and infrastructure projects.

The rise in borrowing costs is now directly impacting government budgets, with interest payments showing a steady upward trend, particularly evident in the United States.

Across developed economies, the amount spent on servicing debt has now surpassed national defence expenditure, underscoring the mounting fiscal strain.

Investor apprehension is also reflected in the increasing "term premiums" observed, especially in US bonds, amid growing uncertainty surrounding fiscal policies, inflation outlooks, and central bank actions.

While some nations, particularly within the Eurozone, have experienced a reduction in borrowing risks following past debt crises, others are encountering renewed financial challenges.

Italy has benefited from enhanced political stability and more effective fiscal management. In contrast, France faces higher risk premiums due to political uncertainty and its budgetary challenges.

Japan's bond market has also faced scrutiny, with weak demand for long-term bonds leading to a sharp rise in yields, prompting authorities to adjust their issuance strategies.

Despite some signs of stabilisation, borrowing costs generally remain under upward pressure, highlighting the precarious state of global public finances.

Comments (0)

You must be logged in to comment.

Be the first to comment on this article!